Why CIS feels different is not really about a slogan.

It is about what happens when a restaurant owner talks to an insurance agency and immediately notices whether the conversation feels generic or relevant.

That difference matters more than ever right now. The National Restaurant Association’s report Persistent Cost Increases and Enduring Demand Will Shape the Restaurant Industry in 2026 says operators are still working through intense pressure from labor, food costs, insurance, energy, and swipe fees. In that kind of environment, a restaurant owner does not need an insurance conversation that sounds broad and theoretical. They need one that feels connected to the real pressure of the business. (restaurant.org)

That is where CIS starts to feel different.

Not because every agency in Florida is bad.

And not because every restaurant needs a dramatic insurance story.

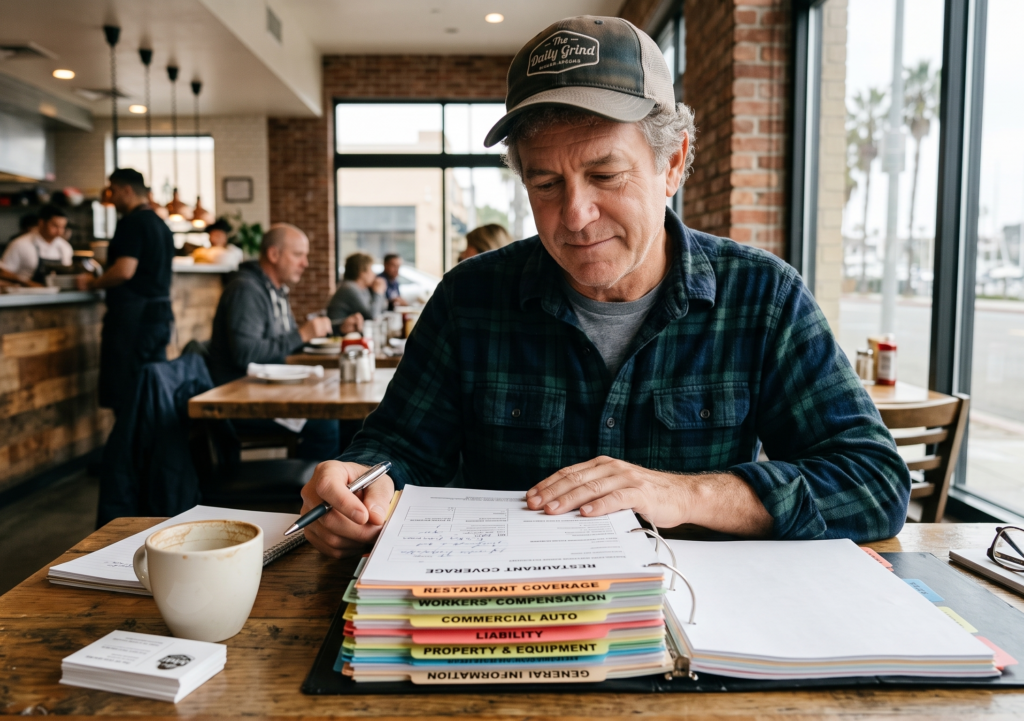

It feels different because CIS presents itself less like a random list of policies and more like a business that actually understands the kinds of risks Florida operators are trying to manage. On the CIS site, the structure itself says a lot. It is not just general insurance language. It clearly highlights Restaurant and Entertainment Insurance, Workers Compensation Insurance, Commercial Auto, Life Insurance, Commercial Liability, and General Liability as visible service lines. (usa-cis.com)

That matters because restaurant owners do not live inside one isolated risk. Their business is layered. The right agency should feel like it understands that from the beginning.

The first difference is that CIS does not feel generic

A lot of agencies can technically insure a business.

That is not the same as feeling built for the kind of business you run.

When a restaurant owner talks to a generalist agency, the conversation can feel too broad. It becomes a talk about “coverage” in the abstract. But a restaurant does not operate in the abstract. It operates through payroll pressure, customer traffic, liquor exposure, kitchen equipment, staff turnover, delivery activity, vendor dependency, and cash flow pressure.

CIS feels different because its site makes a very direct statement about specialization. The Restaurant and Entertainment Insurance page says, “We specialize in providing insurance solutions for restaurants and entertainment businesses. We understand that these industries face unique risks and challenges, and that’s why we’re here to help you protect your business.” (usa-cis.com)

That is a stronger starting point than a generic promise.

It tells the restaurant owner:

you are not walking into a conversation where your business has to be translated first.

CIS feels different because the restaurant is not treated like a side category

This is a subtle point, but it matters.

Many agencies can quote restaurant insurance. That does not mean restaurants are central to how they think. Sometimes the restaurant is just one more account type sitting next to everything else, with no real feeling that the agency understands how layered the operation really is.

CIS looks more deliberate than that. The Restaurant and Entertainment Insurance page does not stop at a vague promise. It lays out multiple relevant coverage areas, including property, liability, Workers’ Compensation Insurance, Commercial Auto Insurance, crime insurance, Cyber Liability Insurance, and Equipment Breakdown Insurance. It also separately highlights Liquor Liability Insurance, General Liability Insurance, and Property Insurance inside the restaurant page itself. (usa-cis.com)

That matters because it changes the nature of the conversation.

Instead of treating the policy like one product, it starts to treat the restaurant like a real operation with multiple moving risks. That is exactly how a restaurant owner thinks when the business is under pressure. They are not thinking about “insurance” as one clean category. They are thinking about the kitchen, the staff, the vehicles, the premises, the alcohol exposure, the guests, the payroll, and the future.

An agency that feels different is usually an agency that starts there.

CIS feels different because the coverage mix actually matches how restaurants live

This is one of the strongest reasons the brand angle works.

A restaurant owner in Florida rarely needs one neat, isolated solution. They usually need a structure.

CIS visibly offers that structure through service lines like Workers Compensation Insurance, Commercial Auto, Life Insurance, Commercial Liability, and General Liability, alongside Restaurant and Entertainment Insurance. (usa-cis.com)

That combination matters because restaurants are rarely exposed in just one way.

A restaurant may need Workers Compensation Insurance because it has employees in a physically demanding environment. It may need Commercial Auto because it has delivery exposure, business-use vehicles, or transport-related risk. It may care about Life Insurance because the owner’s family and long-term planning are tied directly to the business. It may need Commercial Liability and General Liability because customer-facing operations always carry third-party exposure.

What makes CIS feel different is not simply that these products exist.

It is that the mix feels closer to how a real operator’s world is organized.

That is a very different feeling from an agency that seems to know only how to quote one line at a time.

CIS feels different because the Florida pressure is real

A restaurant owner in Florida is not shopping for insurance in a vacuum.

They are shopping while dealing with cost inflation, labor issues, insurance pressure, operating volatility, and all the uncertainty that comes with running a hospitality business in a state exposed to storms, lawsuits, staffing problems, and seasonal shifts.

That is why the industry context matters so much. Persistent Cost Increases and Enduring Demand Will Shape the Restaurant Industry in 2026 is not just a headline. It describes the kind of environment where operators need smarter partners, not just cheaper paper. The National Restaurant Association says the business is still under significant strain, with profitability pressure remaining a serious issue. (restaurant.org)

In that kind of market, CIS feels different because its public-facing structure is not telling the owner, “Here is one random policy.” It is telling the owner, “We understand you may need multiple protection angles working together.”

That is a better fit for the actual restaurant reality.

CIS feels different because it sounds like a partner, not just a quoting machine

This is another reason the distinction works.

A lot of insurance experiences feel transactional.

You ask for a quote.

You get a number.

You compare.

You renew later.

And that is the whole relationship.

CIS presents itself differently. On the Contact Us page, it says, “Our team is here to help and answer any questions you may have.” The blog also invites prospects to “Speak with one of our knowledgeable agents and discover how we can help you find the perfect insurance coverage for your needs.” (usa-cis.com)

That tone matters more than it may seem.

Restaurants do not usually need only a number. They need clarity. They need context. They need someone who can help them think through what matters if the business changes, grows, adds vehicles, expands staff, leans harder into alcohol, or faces a difficult claim situation.

When an agency feels different, it often begins with whether it sounds like it expects a relationship or just a transaction.

CIS feels different because it does not stop at restaurant coverage

This is important because restaurant owners are not just restaurant owners.

They are also employers.

They may also be drivers or fleet users.

They may also be family breadwinners.

They may also own property.

They may also be thinking about long-term personal and business protection at the same time.

That is why a broader menu matters. On the CIS site, Life Insurance says, “We specialize in providing life insurance solutions to protect your loved ones and your assets.” It also says, “CIS provides unique services that achieve peace of mind for each of our clients.” (usa-cis.com)

That may sound like a separate category, but it is actually part of what makes the agency feel different. A restaurant owner is rarely solving only one problem at a time. If the same agency can speak to both business and personal protection in a coherent way, the relationship starts to feel more useful.

That is one reason the direct commercial angle works here:

CIS does not only look like a place where you buy a restaurant policy.

It looks like a place where you can build a more complete protection structure.

CIS feels different because it makes the “why” easier to understand

A lot of insurance communication feels too abstract.

It talks about protection in language that does not help the owner understand why the policy mix matters.

CIS’s restaurant page is more useful than that because it shows the logic of the structure. The Restaurant and Entertainment Insurance page explicitly breaks out coverage areas like Liquor Liability Insurance, General Liability Insurance, and Property Insurance, which helps the owner see that restaurant risk is not one big blur. (usa-cis.com)

That matters because clarity builds trust.

A restaurant owner wants to feel that the agency sees the business in pieces that make sense:

- the building and equipment

- the guests and third-party exposure

- the alcohol exposure

- the employees

- the vehicles

- the digital side

- the interruption risk

- the owner’s long-term protection

CIS feels different because the way it presents itself already hints at that logic.

CIS feels different because it is easier to imagine growing with it

One weakness of generic agencies is that they may be fine for a simple starting point but feel less useful as the business gets more complicated.

A restaurant that starts adding more staff, more alcohol sales, more delivery activity, or more operational complexity may outgrow an agency that never really understood the model in the first place.

CIS feels different because its visible service structure already suggests a business owner can grow into a broader insurance relationship instead of starting over every time the operation evolves. Workers Compensation Insurance, Commercial Auto, Life Insurance, Commercial Liability, and Restaurant and Entertainment Insurance are not unrelated categories on the site. For a business owner, they are often connected categories. (usa-cis.com)

That makes a difference.

The right agency should not only protect the business you have now.

It should still make sense when the business changes.

CIS feels different because it feels more focused on business reality than on insurance language

This may be the biggest difference of all.

Restaurant owners are busy. They do not want a lecture on policy vocabulary. They want to know that the agency understands the reality of:

- employees getting hurt

- customers making claims

- vehicles creating exposure

- equipment breaking down

- margins getting tight

- storms disrupting operations

- ownership risk extending into personal life

That is why the CIS positioning works. The About Us page says CIS offers “a comprehensive range of insurance products” and aims to provide “tailored solutions that offer maximum coverage at competitive rates.” (usa-cis.com)

Those phrases matter because they get to the heart of what a business owner wants:

not just more policy language, but a structure that feels tailored, complete, and commercially sensible.

That is ultimately why CIS feels different.

Not because it promises magic.

Not because it says other agencies are useless.

But because it presents itself like a business that actually expects the client’s risks to be layered and specific.

The sharper conclusion

So why does CIS feel different from other insurance agencies in Florida?

Because it does not seem to approach the restaurant owner as a generic prospect with one policy need.

It approaches the owner more like a real operator with interconnected risks.

That is visible in the way CIS highlights Restaurant and Entertainment Insurance rather than burying restaurants inside a generic commercial bucket. It is visible in the way it pairs that with Workers Compensation Insurance, Commercial Auto, Life Insurance, Commercial Liability, and General Liability. It is visible in the way the site talks about tailored solutions, knowledgeable agents, and a broader protection structure. (usa-cis.com)

And in a year where Persistent Cost Increases and Enduring Demand Will Shape the Restaurant Industry in 2026, that difference is not cosmetic. It matters. (restaurant.org)

Because when margins are tight and the business is exposed from multiple angles, a restaurant owner in Florida does not just want insurance.

They want an agency that feels like it understands the business.

That is why CIS feels different.