There is a reason the story of the 16 bars and restaurants matters.

It is not only because they won.

It is because their case exposed one of the hardest truths in business insurance: a policy can look like protection for years, and then in one historic crisis, the entire future of the business may depend on a few words that nobody took seriously enough when times were normal.

That is what makes this such a good story for restaurant owners.

In December 2024, the North Carolina Supreme Court ruled that Cincinnati Insurance had to cover the losses of 16 bars and restaurants that were shut down in the early stage of the COVID-19 pandemic. Reuters reported that the court found the policy language ambiguous and, under North Carolina law, interpreted that ambiguity in favor of the policyholders. Reuters also noted that the ruling went against the broader trend in many federal and state courts, which had usually sided with insurers in pandemic business-interruption disputes.

That makes this more than a legal curiosity. It makes it a business lesson.

Because the story is not really about COVID anymore.

It is about what owners assume a policy means, what it actually says, and what happens when survival depends on that gap.

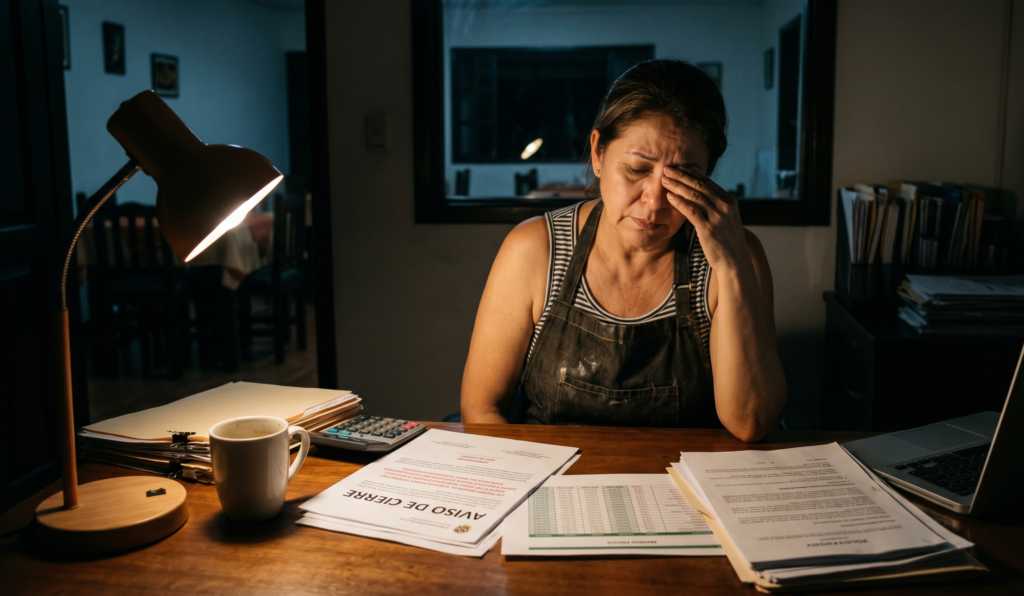

At first, this looked like the kind of loss many owners could not survive

If I tell this story the right way, it does not begin in a courtroom.

It begins in the kind of silence restaurant owners still remember from 2020: closed dining rooms, staff uncertainty, bills still arriving, and owners staring at a business that was no longer allowed to operate normally.

That is why the case resonates so deeply.

For those 16 bars and restaurants, the issue was not theoretical. It was not an academic coverage debate. It was a question that many businesses faced in one form or another:

If the doors are shut, the revenue stops, and the expenses keep going, what exactly is the insurance policy worth now?

That is the emotional center of the story.

Owners buy insurance because they think it will matter in the wrong moment. Then the wrong moment comes, and the whole issue becomes whether the policy was written clearly enough to protect them when it counted.

CIS already touches that broader lesson in business interruption insurance: a must for restaurants, where it says business interruption insurance is designed to protect restaurants from the financial fallout of operational downtime and can help cover lost income, payroll, rent, and utilities after covered shutdowns. (usa-cis.com)

The story of the 16 bars and restaurants matters because it shows what happens when business owners discover that the promise of interruption coverage may rise or fall on the language inside the policy.

The heart of the case was not emotion. It was wording.

That is what makes this story powerful for a CIS audience.

Reuters reported that the North Carolina Supreme Court ruled for the policyholders because the policy language was ambiguous. That ambiguity, the court said, had to be interpreted in favor of the insured businesses under North Carolina law. Reuters also said the decision stood apart from the “bandwagon” of decisions that had largely favored insurers on pandemic shutdown claims.

That is the key lesson:

The outcome did not turn only on sympathy for struggling restaurants.

It turned on wording.

That should make every restaurant owner pay attention.

Because in ordinary times, a lot of owners treat policy wording like something technical and distant. They care more about price, renewal, or whether the certificate is in place. That is understandable. Running the restaurant already takes enough attention.

But stories like this expose the cost of that mindset. If a policy has vague language, undefined terms, or important gaps that nobody really studies, those details can become the whole battle when the business needs protection most.

Why this story hits so close to home for restaurants

Restaurants do not need many weeks of shutdown to feel real danger.

That is what makes this case so usable in content for CIS.

A lot of businesses can survive disruption better than restaurants can. Restaurants are unusually vulnerable because they often operate with:

- thin margins

- perishable inventory

- heavy payroll pressure

- lease obligations

- fixed overhead that does not disappear during closure

- a business model built on steady traffic and momentum

That is why the central question in a shutdown is so brutal:

if the business cannot operate, who absorbs the financial shock?

CIS already builds around that logic in what should a restaurant do to avoid bankruptcy, where it argues that restaurants usually fail when several pressures stack up and the business no longer has enough room to absorb them. (usa-cis.com)

The story of the 16 bars and restaurants turns that logic into a real case. The insured businesses did not simply want a symbolic win. They needed the coverage dispute to go their way because interruption losses can threaten the survival of a restaurant much faster than many owners want to admit.

This case mattered because most similar cases did not go this way

That is another reason this story is so strong.

Reuters made clear that this was not the ordinary result. In fact, it reported that the ruling contradicted decisions from 11 federal circuit courts and more than 20 state supreme courts that had usually sided with insurers on pandemic-related business interruption claims.

That detail matters because it gives the story tension.

This was not a routine outcome.

These businesses were not just surfing the general tide.

They won in a landscape where many others had lost.

That makes the lesson sharper, not weaker.

It means restaurant owners should not take away the simplistic message that every shutdown claim is automatically covered. The better lesson is more precise and more valuable: when coverage turns on language, wording can become decisive, and businesses that assume too much about their policies may not realize how exposed they are until the dispute is already underway.

That is exactly the kind of sober point CIS should want to make.

The real story is not “the courts saved them”

A weaker version of this article would turn the case into a triumph story and stop there.

That would miss the deeper value.

The real lesson is not that owners should hope for a heroic court result someday. The real lesson is that insurance decisions should be made with enough care that the business is not depending on luck, ambiguity, or years of litigation to survive.

Because even in a case where the insured businesses ultimately won, think about what that means in human terms:

- the shutdown already happened

- the financial pain already happened

- the uncertainty already happened

- the legal fight already happened

- the wait already happened

So the smartest use of this story is not “look, they won.”

It is “look how much depended on policy language once the crisis had already arrived.”

CIS already leans in that direction in insurance insights for restaurant business owners, where it says business interruption insurance helps a restaurant focus on reopening rather than financial strain when temporary closure hits. (usa-cis.com)

The case of the 16 bars and restaurants gives that advice a harder edge:

the business cannot count on interruption protection if the wording was never fully understood in the first place.

This is why owners should care about ambiguity before a crisis, not during it

One of the hardest business lessons is that ambiguity feels harmless until the business needs certainty.

A vague clause can sit quietly inside a policy for years. During those years, the owner pays, renews, and moves on. Nothing forces the uncomfortable questions.

Then a crisis comes.

Operations stop.

Cash flow tightens.

And suddenly the vague clause becomes the center of the entire survival conversation.

That is why this story should connect directly to key questions for reviewing your restaurant insurance plan. The whole point of that CIS article is that owners should ask the hard questions before a claim or shutdown forces them to. (usa-cis.com)

The 16 bars and restaurants are the real-world proof of why that matters.

They are a reminder that a policy review is not a bureaucratic exercise. It is one of the few moments where a business can discover whether its assumptions are weak before reality tests them.

For restaurant owners, this is not just a pandemic story

That point is worth underlining.

A lot of owners will read a COVID case and think: that was a strange historical moment, interesting but not really relevant now.

That is too narrow.

The durable lesson is about interruption, closure, uncertainty, and disputed coverage. Pandemic shutdowns may have been unusual, but restaurants still face many situations where operations can be disrupted and the owner suddenly needs the policy to mean something concrete.

That is why business interruption insurance: a must for restaurants remains relevant even though the pandemic years are behind us. CIS explains there that interruption coverage helps bridge the financial gap when a restaurant cannot operate normally after a covered event. (usa-cis.com)

The broader lesson from the 16 bars and restaurants is this:

interruption risk is real, and the strength of your position may depend on how the policy is written long before the interruption ever happens.

What this story should make a Florida restaurant owner ask

If a Florida restaurant owner reads this story correctly, it should create a more disciplined kind of anxiety.

Not panic.

Not false confidence.

Better questions.

For example:

- Do I actually understand what my policy says about interruption?

- Which shutdown scenarios are clearly addressed, and which are not?

- Are there exclusions or undefined terms I have never really asked about?

- Have I reviewed the business the way a dispute would review it?

- If operations stopped under a stressful scenario, would my current coverage structure be as clear as I think it is?

That is where restaurant and entertainment insurance also belongs in the conversation. CIS frames restaurant protection as layered because the real business is layered: liability, property, workers’ compensation, cyber issues, equipment breakdown, and interruption concerns can overlap fast. (usa-cis.com)

The 16 bars and restaurants story is really about what happens when one of those layers becomes the deciding factor.

The deepest lesson is not legal. It is strategic.

This may be the most useful line in the whole article:

The deepest lesson is not legal. It is strategic.

The businesses in this case did not just get lucky because a court liked their story. They benefited from the fact that the wording issue gave them a path to argue that coverage existed. Reuters said the court found the language ambiguous and interpreted it for the insured businesses.

That should make every owner think more strategically about insurance.

A policy is not just a document you keep around for proof.

It is a piece of business infrastructure.

And infrastructure only proves its value when pressure hits it.

This is why CIS should keep pushing owners to think beyond the premium number. A cheaper policy that leaves dangerous ambiguity or weak protection around interruption can become much more expensive later if the business is forced into a fight when cash flow is already under pressure.

This story also explains why so many owners feel betrayed after a denial

There is another emotional layer here that matters.

Many owners do not read a denial as a technical contract disagreement. They experience it as betrayal.

From their perspective, they paid for years. They thought they were doing the responsible thing. Then the wrong event happened, and suddenly the insurer’s interpretation feels narrower than the owner ever imagined.

That emotional reality is part of why cases like this resonate so much.

The 16 bars and restaurants probably did not think of themselves as launching a landmark legal theory. They thought they had suffered losses and wanted the policy to respond. That is exactly how many owners think: not like coverage lawyers, but like operators.

Which is why stories like this should push restaurant owners to stop treating policy review as something that can always wait.

The sharper conclusion

So why should a restaurant owner care about the story of the 16 bars and restaurants?

Because it proves something most people only learn under pressure:

The value of insurance is not tested when you buy it.

It is tested when the business is hurting and the wording suddenly matters more than your assumptions.

Reuters reported that these businesses won because the North Carolina Supreme Court found the language ambiguous and interpreted it in their favor. That is a real victory. But it is also a warning.

A restaurant should not have to discover the meaning of its protection only after operations stop and the financial pressure is already on.

That is the real lesson.

The story is not just that 16 bars and restaurants fought for coverage.

It is that they remind every owner why policy wording deserves attention before the next crisis decides everything.