Restaurant Insurance

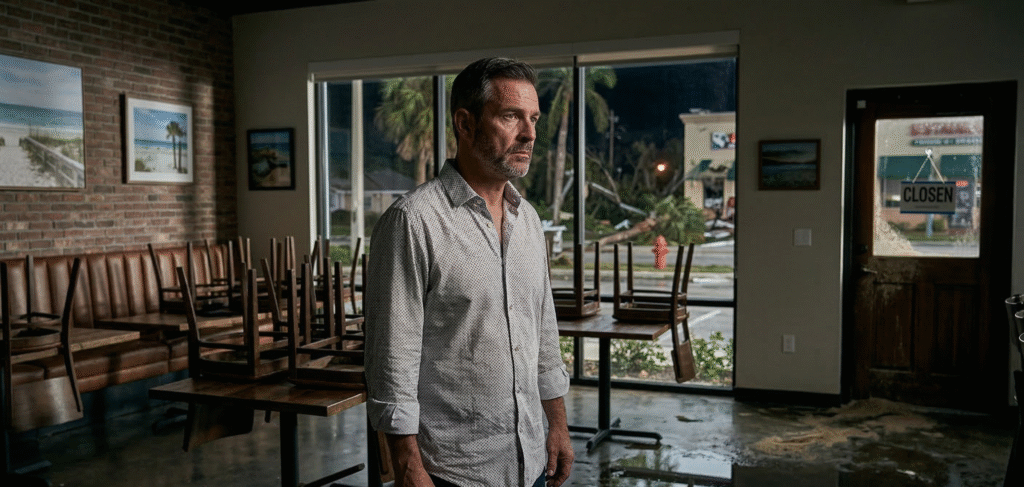

If you run a restaurant in Florida, you already know storms are not an abstract risk. They are part of the operating environment. You plan for inventory, staffing, vendors, equipment failures, and customer demand. But one of the hardest situations to absorb is the one that stops the business itself: a storm forces the restaurant to close.

That kind of closure creates a very different kind of pressure. It is not only about broken windows, roof leaks, water intrusion, or damaged equipment. It is also about the income that disappears while expenses continue. Payroll pressure does not magically vanish. Rent usually does not stop. Vendors may still need answers. Refrigerated or frozen inventory can be lost. Customers move on quickly. Reopening almost always takes longer than owners hope.

That is why storm-related shutdowns hit restaurants so hard in Florida. The physical damage is only the first layer. The deeper threat is operational interruption.

This matters because Florida businesses are repeatedly encouraged by emergency management and preparedness agencies to build continuity plans before disasters happen, not after. Ready.gov’s business preparedness resources emphasize continuity planning for hazards including hurricanes, flooding, and power outages, while the Florida Division of Emergency Management specifically advises businesses to keep continuity plans updated and ensure employees understand their responsibilities during disasters.

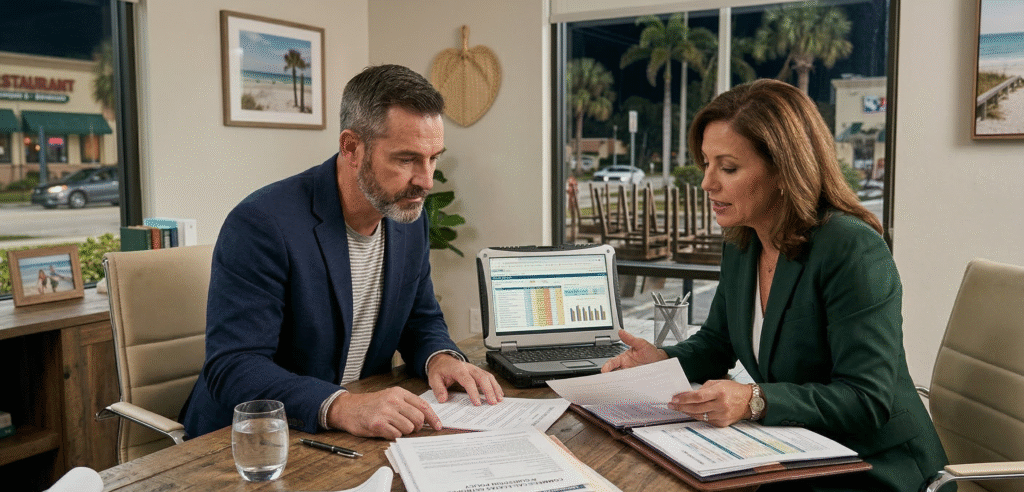

For restaurant owners, that means protection is not just about repairing the building. It is about understanding what a closure really costs, what types of insurance may matter most, and where dangerous gaps often appear.

Why Restaurant Closures After Storms Are So Financially Dangerous

A lot of business owners naturally focus first on visible damage. That makes sense. If part of the building is damaged, if water got inside, if signage is destroyed, or if refrigeration systems fail, those are urgent problems.

But for restaurants, the real pain often comes from how many systems depend on the doors staying open.

A storm closure can affect:

- daily cash flow

- scheduled reservations or events

- payroll obligations

- perishable food inventory

- vendor deliveries

- staffing stability

- customer trust and routine traffic

- cleanup and reopening timelines

Restaurants are especially vulnerable because they usually work with narrower daily margins than many people realize. One week of closure may feel very different from one week of inconvenience. If the restaurant depends on regular turnover, lunch volume, delivery traffic, or weekend business, downtime can become a serious financial event very quickly.

This is one reason Florida emergency planning guidance matters so much for hospitality businesses. State business preparedness resources are built around the reality that hazards can threaten operations and economic continuity, not just physical property.

Storm damage is often recoverable. The harder question is whether the business can absorb the interruption long enough to recover well.

The Difference Between Property Damage and Business Interruption

This is where many restaurant owners get surprised.

They assume that if storm damage is covered, the problem is largely solved. But property damage and business interruption are not the same thing.

Property damage usually concerns the physical part of the loss:

- roof or structural damage

- broken glass or signage

- damaged kitchen equipment

- ruined furniture or fixtures

- water intrusion into walls, flooring, or storage areas

Business interruption is different. It is about what happens because the restaurant cannot operate normally.

That may include:

- lost revenue during closure

- continuing fixed expenses

- income reduction during partial reopening

- operational disruption tied to covered physical loss

The distinction matters because many owners think first about repairs and only later realize the deeper loss was the inability to generate revenue while the business remained closed.

For a restaurant, that lost operating time can be more painful than the initial repair bill.

What Storm Closures Usually Look Like in Real Life

The idea of “closing after a storm” sounds simple until it happens. In practice, it can happen in several ways.

1. Direct physical damage

A hurricane, tropical storm, or severe weather event damages the structure, roof, windows, signage, outdoor seating, or internal equipment. The restaurant cannot reopen until repairs or cleanup are completed.

2. Water intrusion and spoilage

The building may remain standing, but water intrusion, ceiling leaks, or flooding damages storage areas, kitchen spaces, or dining areas. Perishable inventory is compromised and operations are no longer safe or practical.

3. Power outage and refrigeration loss

Even without dramatic structural damage, a prolonged outage can shut down refrigeration, ice production, ventilation, POS systems, and normal food handling. In many restaurants, that alone can force temporary closure.

4. Access and safety disruption

Road closures, local emergency orders, debris, or neighborhood damage may make access unsafe or impractical for staff and customers. The restaurant may technically still exist, but it is not functioning as a business.

5. Delayed reopening because of cleanup and supply chain issues

Some businesses assume they will reopen quickly once the storm passes. In reality, cleanup crews, equipment replacement, inspections, contractors, and vendor timelines can delay reopening longer than expected.

This is why business continuity planning cannot be treated like paperwork. Ready.gov and Florida emergency management materials repeatedly emphasize planning ahead for operational continuity rather than improvising after an event.

Why Florida Restaurants Face More Operational Exposure Than Many Other Businesses

Not every business absorbs storm-related closure the same way. Restaurants face a different level of fragility for several reasons.

First, they depend heavily on physical space. If the kitchen, dining room, refrigeration, ventilation, plumbing, or front-of-house systems are compromised, the business often cannot function at even a reduced level.

Second, they depend on perishables. Storm-related power loss, water intrusion, or sanitation issues can make inventory unusable fast.

Third, they depend on rhythm. Customer habits are fragile. If a restaurant closes unexpectedly, some customers will come back, but some will shift immediately to competitors.

Fourth, many restaurants rely on a blend of dine-in, pickup, delivery, catering, and event-based revenue. Storms can interrupt several of those channels at once.

Fifth, staffing becomes unstable during closures. Employees may lose shifts, seek temporary alternatives, or become unavailable due to their own storm-related circumstances.

That combination makes restaurant shutdowns especially costly. The business is not just waiting for repairs. It is trying to preserve momentum, customer trust, and team continuity at the same time.

Where Coverage Gaps Usually Show Up

This is the part owners often discover too late.

A storm hits. Damage occurs. The restaurant closes. The owner assumes the policy will carry the business through. Then the questions begin.

- Was the damage caused by a covered peril?

- Does the policy structure match the actual operation?

- Are limits high enough for replacement costs?

- Is downtime addressed clearly enough?

- Was spoilage considered?

- Were there exclusions that matter now?

- Were all parts of the location properly valued?

Coverage gaps tend to show up in a few common places.

Underinsured property values

Replacement and repair costs rise over time. If limits do not reflect current realities, owners may discover that the property is not insured as fully as they thought.

Business interruption misunderstandings

Some owners assume interruption protection automatically applies in every closure scenario. In practice, the trigger and structure matter.

Food spoilage and equipment-related losses

Restaurants are more exposed to perishable loss than many other businesses, but not every owner reviews that issue with enough specificity.

Outdoor and ancillary assets

Outdoor seating, patio elements, signage, decorative structures, or entertainment-related fixtures may be more important to the business than a generic policy assumes.

Operational evolution

If the business changed over time, added alcohol service, delivery, events, catering, or new equipment, the original policy may no longer reflect the real operation.

This is exactly why restaurant-specific protection matters more than generic small business coverage. CIS’s own restaurant and entertainment insurance page highlights the need for a broader mix of protections, including general liability, property, liquor liability where relevant, and operationally appropriate coverage built around hospitality risk.

The Hidden Cost of Reopening Slowly

Many owners think in terms of one question: “Will we be covered?”

The better question is often: “How expensive will a slow reopening become?”

That is a harder question because the losses are not always neat.

A slow reopening can mean:

- reduced customer return

- lower staff morale

- temporary menu limitations

- canceled events or reservations

- vendor complications

- reputation damage if communication is poor

- higher cleanup and restart costs

In some cases, reopening halfway can create a different type of pressure. The restaurant may technically be open, but not fully functional. Capacity may be reduced. Equipment may still be missing. The menu may be limited. Delivery may be paused. The business is back, but not truly back.

That gray zone can be financially exhausting.

From a risk-management perspective, one of the biggest benefits of smart insurance planning is not just surviving the initial event. It is making recovery less chaotic and less financially destabilizing.

Why Continuity Planning Matters as Much as Insurance

Insurance is critical, but it is not the whole answer.

A restaurant that has good coverage but no continuity plan can still reopen poorly. A restaurant that has some continuity planning but weak coverage can still face major financial damage. The strongest position usually comes from combining both.

Business preparedness resources from Ready.gov include hazard-specific tools for hurricanes, flooding, power outages, and severe weather, while Florida’s business planning guidance specifically encourages keeping continuity plans current and making sure team members understand responsibilities.

For restaurants, a real continuity plan should usually address:

- emergency staff communication

- shutdown procedures

- inventory protection steps

- refrigeration contingency planning

- vendor coordination

- documentation of damage

- backup records and financial access

- reopening workflow and priorities

This is not theoretical. The faster the owner can assess damage, communicate clearly, document losses, and move toward safe reopening, the more survivable the closure becomes.

Insurance can help absorb financial shock. Planning helps reduce operational chaos.

The Restaurant Insurance Conversation Most Owners Need Earlier

A lot of owners do not review this part of their insurance until after they have already experienced at least one painful disruption.

That is understandable. Storm planning is not the most exciting part of running a restaurant. Owners are busy, margins are tight, and many urgent problems feel more immediate.

But in Florida, weather exposure is not a fringe issue. It is a recurring business reality. State preparedness guidance is built around that assumption, and restaurant owners should probably treat it the same way.

A useful review usually includes questions like:

- If a storm shut us down for a week, what would hurt most financially?

- If we lost power and inventory, do we know what part of that loss is covered?

- If part of the building was damaged, how long could we carry fixed costs?

- Has our restaurant changed enough that our older policy setup may no longer fit?

- Are we relying on assumptions instead of documented coverage review?

These are not pessimistic questions. They are strategic questions.

The businesses that ask them early tend to make better decisions when it matters.

Why Generic Small Business Thinking Can Be Dangerous for Restaurants

One of the mistakes we see in internal SEO content again and again is when restaurant owners compare their risk too casually with “small business” risk in general.

Restaurants are not generic.

They combine:

- physical premises exposure

- high customer traffic

- employee injury risk

- perishable inventory

- sanitation pressures

- time-sensitive operations

- equipment dependence

- weather sensitivity

- sometimes alcohol-related exposure

- sometimes delivery-related exposure

That stack of risk means closures hit harder and recoveries can be more complex.

This is also why broader commercial liability conversations matter even when the storm itself seems like a property issue. Once operations are disrupted, other forms of exposure can follow — customer injuries during reopening, vendor disputes, access issues, or operational incidents tied to damaged conditions. CIS’s commercial liability page emphasizes third-party injury and damage exposure as a core protection issue for businesses operating with public interaction.

Restaurants need a more deliberate insurance structure because their interruptions are rarely simple.

What a Smarter Review Looks Like Before Hurricane Season

A strong pre-season review does not have to be overwhelming. It just has to be honest.

A restaurant owner should be able to answer practical questions such as:

- What parts of our location would cost the most to repair or replace?

- What are the most likely reasons we would be forced to close after a storm?

- Which revenue channels would stop first?

- How much inventory is exposed to spoilage risk?

- How quickly could we document losses and make decisions?

- Are our current property values and limits still realistic?

- Have we reviewed interruption issues with the business model we run today?

Florida hurricane preparedness guidance consistently encourages advance preparation, supplies, communication planning, and business readiness before the season escalates.

For restaurants, that planning should include insurance review, not just shutters and generators.

What Owners Often Regret Most After a Storm

After a storm-related shutdown, regret usually sounds like this:

- “I thought we were covered.”

- “I didn’t realize downtime would hurt this much.”

- “I wish we had reviewed the policy before the season started.”

- “I didn’t think about spoilage or reopening delays.”

- “I assumed we’d be back in a day or two.”

That last one matters a lot. Reopening timelines are often longer than owners imagine, especially when contractors, inspections, utility restoration, cleanup crews, and replacement equipment are all involved.

That is why the most useful restaurant insurance conversations are not the ones held during the claim. They are the ones held before the event.

Final Thoughts: Storm Damage Is Only Half the Story

For a Florida restaurant, the real danger of a storm closure is not only what gets damaged. It is what stops moving.

Cash flow stops.

Routine stops.

Customer traffic stops.

Events stop.

Normal operations stop.

And the longer that pause lasts, the more expensive the closure becomes.

That is why storm-related planning has to go beyond physical repairs. Restaurant owners need to think in terms of continuity, downtime, spoilage, staffing pressure, and recovery speed. They also need to think carefully about whether their current insurance setup reflects how the business actually operates today, not how it looked a year or two ago.

If there is one takeaway that matters most, it is this: in Florida, storms should not be treated like rare surprises. They should be treated like real operational risk.

The better a restaurant understands that risk in advance, the better chance it has not only to survive a closure, but to recover without losing more than it should.